- 1300 136 917

- admin@bcadebt.com.au

- Mon - Fri 8.30 am to 4.30 pm

How to sign up for debt collection services

Signing up for our services.

To start with, you need to select the industry you are in on this link https://www.bcadebt.com.au/debt-collection and enter your details. This takes you to the pricing page and the links to register.

On the link, enter all the details of your business. Once you have done this, you will be directed to add your first debt.

The Six Step Debt Collection Process

This process is designed to encourage a resolution of the debt within three months. If there is no resolution by then your collector will make a determination to continue the process for a further three months based on the likelihood of the debt being recoverable.

BCA Debt follows this process stringently to ensure that every possibility is explored to get the best outcome. Further information is found in the client guide which outlines all the requirements of a successful debt collection.

Things to take into consideration

- All steps here are performed at the collector's discretion and may not flow in the exact order;

- Some steps will organically be left out of the debt collection process as they are not always necessary.

- Debt collection is an emotionally-charged process and the collectors are trained to manage this emotion and perform accordingly.

Step 1 First contact

Once a debt is entered into the system, we make first contact via a letter of demand by email and a phone call using the contact information provided.

When the debtor responds there are three options.

- The collector enters negotiations for the payment in full.

- Or by payment arrangement.

- Discusses any disputes or problems that have occurred with the product or service with the debtor.

If no response, the collector will move to step two.

Step 2 Debtor Contact

See ACCC/ASIC Debt Collection Guidelines. This is imperative reading as there are restrictions as to when and who a collector or creditor can implement the following procedures.

Contacts include:

- Speaking to the debtor by phone.

- Letters sent to the debtor (BCA Debt has a series of letters that are utilised after the Letter of Demand has been issued).

- Emails.

- SMS.

- Phone messages.

A minimum of 6 contacts are made per month; if no contact is made a further 4 contacts are attempted. No more than 10 contacts per month can be made. This is in accordance with the ACCC/ASIC Debt Collector’s Guidelines.

Step 3 Negotiations

Please refer to your client guide for information in regard to negotiated debts. Also, see ACCC/ASIC Debt Collectors Guidelines in regards to providing information and documents to your collector when requested. Failure to do so may constitute misleading and deceptive conduct.

- Collectors negotiate with debtors in regard to the payment of debt.

- Negotiate payment arrangements.

- Discuss disputes with the debtor and the client to come to a resolution.

- Negotiation of debt adjustments in cases where the client or debtor has made an offer. This will be discussed with the client.

- Research and obtain evidence of any misconduct on either side to effect a resolution to the debt being finalised.

- Follow the procedure for hardship. Customers who are in hardship are asked to provide us with documents that support this.

Step 4 Locating Persons

If the letter of demand is returned or the phones are disconnected the collectors then utilise paid, in-house databases and searching systems to locate the debtor. (This is a complimentary service)

- We match all data supplied with information available within BCA Debt’s resources, telephones, addresses, related names and similar spelling.

- Double-check details to confirm the spelling of addresses.

- Confirm that the individual is not deceased or incarcerated.

- Cross-reference between ABN & ASIC.

Step 5 Paid Skip Trace/Investigation:

Further information is sought in regard to the debtor such as business names, aliases, property ownership, partnerships, bankruptcy and insolvency.

Please note if paid searches are required there will be a minimum fee of $330.00 for skip tracing. Your collector will request this if it is agreed upon. with this step, we utilise a professional investigator and this will take place after 3 months of debt being on our database.

Step 6 Person/Field Call:

The Collector may recommend a Personal Call be issued to a debtor if they are not getting any response from them; they may need to verify the debtor’s current residential address or place of work for papers to be served. The personal call involves a Mercantile Agent making a visit to the nominated address of the debtor and handing them a letter of NOTICE OF INTENTION TO SERVE A GENERAL PROCEDURES CLAIM. The agent is also given instructions on what to discuss with the debtor and demand payment on the account.

There is a fee for the client to pay to have this service and the collector will request this if it is agreed upon.

Legal Action or Write-Off:

Each debt is different and may require different actions. If the client agrees to proceed with the legal process, authorisation paperwork is required to be filled in and returned. If no legal action is required, the debt will be written off.

We only take debts through the legal process if they are over $10000 and we are confident they can be collected. There is also an additional fee and money will be requested to be held in trust.

Note: residential property debts for rentals are not included in the legal action process

Whats included in the price

save

Adding debt collection fees

Adding debt collection costs to your debts.

You can add the costs of going to debt collection to the original invoice amount, and while there are no guarantees, our complete focus will be to collect 100% of the debt ... in which case your debt collection has been free!

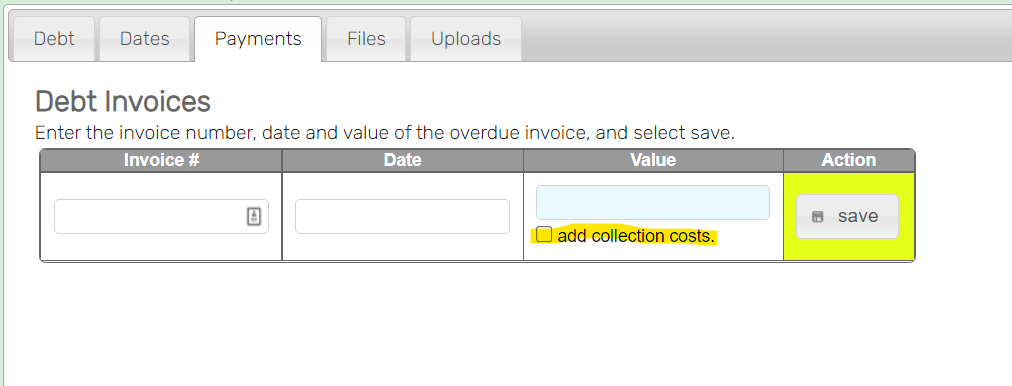

When adding the debt, enter the invoice number, date and value of the overdue invoice. Select add collection costs and the system automatically adds the costs to the debt amount.

Make sure you check the box to add the costs.

Adding your debt

The following is a simple tutorial on adding a debt to our system:

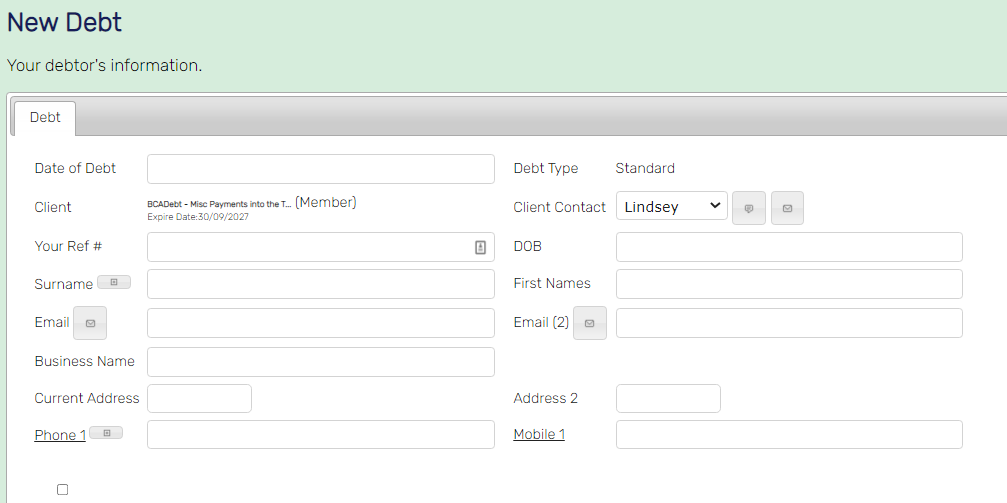

- Once you have logged in to the website, hover over "debts" in green text at the top of the screen and select "add a new debt."

- Now you can enter all the debtors' information in the relevant fields, click to acknowledge your responsibility and save.

- The next step is to upload your files and invoices. This makes the process so much smoother as we will need evidence of the debt.

- Then you will be taken to the "Debt Invoice" page for your debtor.

Enter the invoice number, date and value of the overdue invoice.

Select add collection costs, and our system will automatically add our collection costs to the debt amount.

While there are no guarantees, our complete focus will be to collect 100% of the debt, in which case your debt collection has been free! - You can continue to add invoices to the same person if they have more than one overdue invoice.

- While on this page, you can scroll down to the notes section where, in the first box, you can drag & drop any relevant files, such as copies of invoices, and in the box below this, you can write notes for your collector.

- If you are Pay as You Go, the last step is to select the Generate Invoice button. We will begin working on your debt when we receive payment for this invoice.

Now select "add a new debt" at the top of the page to repeat the process and add another debt.

Client Guide - Ask Your Collector

Your collector is here to help you, any questions that are asked in the process of debt collection are for your collector to gain knowledge on the debt, we have compiled a series of articles based on information required by your collector to perform their role and have a smooth outcome.

The collectors' job is to Limit your Losses.

Client and collector communication

It is imperative that all communication with your debtor is channelled back to your collector and that you do not make any arrangements with your debtor without consulting your collector. This is important as you may weaken the power of your collector by contradicting anything they may have discussed with the debtor and the debt may then be deemed compromised.

- The best method of communication is via the client access system and this should be your first point of enquiry

- Your collector will make notations for you to read every time they access your debt.

- Your collector may contact you via telephone or email for details or any clarification that may be needed.

- Please remember that time spent on the phone to you with enquiries that could be answered by you accessing the web is time spent away from collecting your debt.

Requesting Information

Request for information from your collector, from time to time your collector will request information to be provided by you, this request may be either verbal or in written form. The collector will provide a date by which the information is required. Normally this will be within five working days. Unless specified otherwise.

Your collector may request further information or copies of invoices/statements regarding the debt as required.

BCA Debt Process for requested information

- Your collector may contact you by phone to request information or discuss your debts.

- Alternately an email may be sent, outlining the nature of the information required, giving you a date due for the return of that information.

- BCA Debt Process for negotiation of Debt – Please note this is the power of debt collection and once your debtor puts an offer on the table all parties need to respond quickly.

- When there is a negotiation on the table, twenty-four hours is the optimum amount of time to ensure a good result.

- In the event your collector does not receive an answer from you within the requested time frame, they may deem your failure to reply as acceptance of the offer.

- Alternatively, they may send a letter to your mailing address or email requesting you respond by a certain date. Failure to respond to this type of request may also be deemed as acceptance of the offer.

- Further to this, failure to provide information may result in the debt being compromised and subsequently closed. The full commission will be charged on the debt.

Your collector is not obliged to submit an offer to you, however, they may do so at their own discretion. (see clause 3(f) of the General Provision of Agreement for Debt Collection)

When will I get my money?

The EOM is completed approximately in the first week of the new month and all payments are allocated to clients electronically and invoices and statements are sent to you via email and a link to log in and view them.

The commission charged is subtracted from the amount collected from your debtor and the balance is paid into the bank account you supplied on the system.

You will receive an email with links to the following documents that detail your payments

Download the files here for the month's information: (these will be links to your docs)

Current Invoice | Current Statement | Invoice Summary | Closed / Written Off |

Understanding the information

It is better to read both the invoice and statement side by side. (Best printed if you have a lot of payments)

- The statement shows the amounts paid off your debt and the cost associated with each payment without GST. At the bottom of the statement is the amount we collected in cash and the overall fee we charge.

- The invoice shows the breakdown of the fee and GST per payment. At the bottom of the invoice is the amount owing. Our system generally deducts the amount owing from the amount collected.

See the amount owing on the invoice.

Because most of our clients use different accounting packages, so please refer to your accountant on how to enter the details on your software.

Writing off a debt

Once a debt is handed to BCA Debt, the collector will proceed to work on it for twelve months from the date the debt was added if after some time working on it, they feel that the debt will never be recovered they will advise you.

Writing off debts is done only after your collector has exhausted all feasible avenues of debt collection.

If this is the case the debt will be closed, and no commission is payable on the balance of outstanding monies.

Will this affect their credit rating?

When your debtor pays the debt in full and it has been removed from our computer system, the credit rating will not be affected.

For a fee, BCA Debt can lodge a Mercantile Enquiry on your debtor this is where a debt is lodged against your customer for the amount you have sent to us. The Mercantile Enquiry lodgement remains on your customer for 5 years. The customer must have an ABN and there are requirements that need to be carried out prior to lodgement.

Adding your debt

The following is a simple tutorial on adding a debt to our system:

- Once you have logged in to Recoveries Global, hover over "debts" in green text at the top of the screen and select "add a new debt."

- Now you can enter all the debtors' information in the relevant fields, click to acknowledge your responsibility and save.

- You will be taken to the "Debt Invoices" page for your debtor. Enter the invoice number, date and value of the overdue invoice. Select add collection costs and our system will automatically add our collection costs to the debt amount. While there are no guarantees, our complete focus will be to collect 100% of the debt, in which case your debt collection has been free!

- You can continue to add invoices to the same person if they have more than one overdue invoice.

- While on this page, you can scroll down to the notes section where, in the first box, you can drag & drop any relevant files such as copies of invoices, and in the box below this you can write notes for your collector.

- This last step is to select the Generate Invoice button. When we have received payment of this invoice we will begin working on your debt.

Now select "add a new debt" at the top of the page to repeat the process and add another debt.

Adding costs

You can add the costs of going to debt collection to the original invoice amount and, while there are no guarantees, our complete focus will be to collect 100% of the debt ... in which case your debt collection has been free!

When adding the debt enter the invoice number, date and value of the overdue invoice. Select add collection costs and the system will automatically add the costs to the debt amount.

When a case goes to court

Our collectors follow a proven debt collection procedure involving different levels and methods of contact. Our policy is to follow this procedure to make sure that the value is there for the client.

If your collector feels that issuing a summons will be an option that is highly likely to get a good outcome, you will be given a quote for the costs of getting your case in front of a magistrate.

Your collector will prepare the majority of the documents, and you will liaise with your collector throughout the court process.

Court action is not taken lightly and a decision is made on the merits of each individual case.

Legal Action– these costs are paid upfront and sent with the court documents & paperwork to BCA’s legal team.

- BCA is unable to provide a quote for legal proceedings; if your collector feels this is an avenue worth taking they will send you the relevant information.

- You are responsible for all ongoing costs in regard to legal proceedings

Taking a debtor to court is only carried out if your collector believes they will get the money back for you, there must be value to doing this process.

For more info read this blog. Debt collection versus going to court

Value for money

- What we do is follow the full debt collection process by using our “Six step debt collection system.” This is designed to get clarity from your customer as to what their attitude is towards the debt and verify with them that they need to pay and we then negotiate payment on your behalf.

- The six-step process is a specially designed program for debt collectors and our collectors are all trained with this system.

- We match the collector with your type of business, and the collector will take over the entire collection process on your behalf leaving you free to concentrate on your profession

- Our team of collectors are highly motivated to get the best outcome for you, they are paid on commission so we don’t get paid if they don’t collect the debt.

- Our online client access system allows you to keep up with what is going on with your debt.

We are affiliated with a National network of Agents who can go to any debtor’s home or - With the national network, we are expected to follow a strict code of conduct and our company prides itself on making sure we follow the debt collection guidelines which protect both you and us.

By following our six-step debt collection process we can assure our clients get value for money in the debt process.

Proof of debt

Proof of debt in collection and legal proceedings lies with the person alleging the debt is owed. Therefore you are responsible to prove that the debtor owes you the money and BCA Debt will require proof of debt to follow debt collection procedures.

Your collector may request further information or copies of invoices/statements regarding the debt as required. When it comes to having a debt collected you need to have proof that a person or entity owes you money. It is your responsibility to prove the debt, not the debtors, to disprove it.

Retrieval of goods

Retrieval of goods, in the case of goods provided, whereby you have a clause in your contract with the debtor stating that goods remain the provider's property until full payment is made.

BCA supports the retrieval of goods when it has been agreed upon by all parties.

It is important to note the changes to legislation in 2012 and the introduction of the Personal Property Securities Act have changed the way in which creditors can enforce the Retention of Title within any contract.

When you have a debt for goods that you have provided you need clear guidance on how to retrieve these, unfortunately, you cannot just go and collect your items there are certain rules that apply.

The six-step debt collection process

This process is designed to encourage a resolution of the debt within a three-month period. If there is no resolution within the three months your collector will decide if they wish to continue the process for a further three months.

Debt collection has a role to maximise you the client in limiting your losses, BCA Debt does not promise at any stage to collect any money whatsoever. BCA Debt promises to follow this process to give clear guidance and satisfaction that every possibility is utilised to get the best outcome, whether the debt is paid or not.

Things to take into consideration

Collectors' rosters are formed around them having the opportunity to follow this procedure. All steps here are performed at the collectors’ discretion and may not flow in the exact order, some steps will organically be left out of the debt collection process as they are not always necessary.

Debt collection is a highly emotionally charged process and the collectors are trained to manage this emotion and perform according to limit the losses of their clients

About adding a debt.

READ THESE BEFORE ADDING A DEBT

CONTACT US

BCA DEBT LOCATIONS

6/8 Edward Street

Bunbury West Australia 6230

(08) 9721 8440

24/77 St Georges Terrace

Perth West Australia 6000

(08) 9221 6098